China's National People's Congress has approved the country's 15th Five-Year Plan, covering the period from 2026 to 2030. The plan, formally passed on 12 March at the close of the annual Two Sessions parliamentary meetings in Beijing, sets the strategic direction for the world's largest emitter across energy, industry, climate and economic policy. For investors, manufacturers and trade partners, the document carries significant weight. It shapes where capital flows in China's industrial economy for the next five years and beyond.

A Clean Energy Push with Caveats

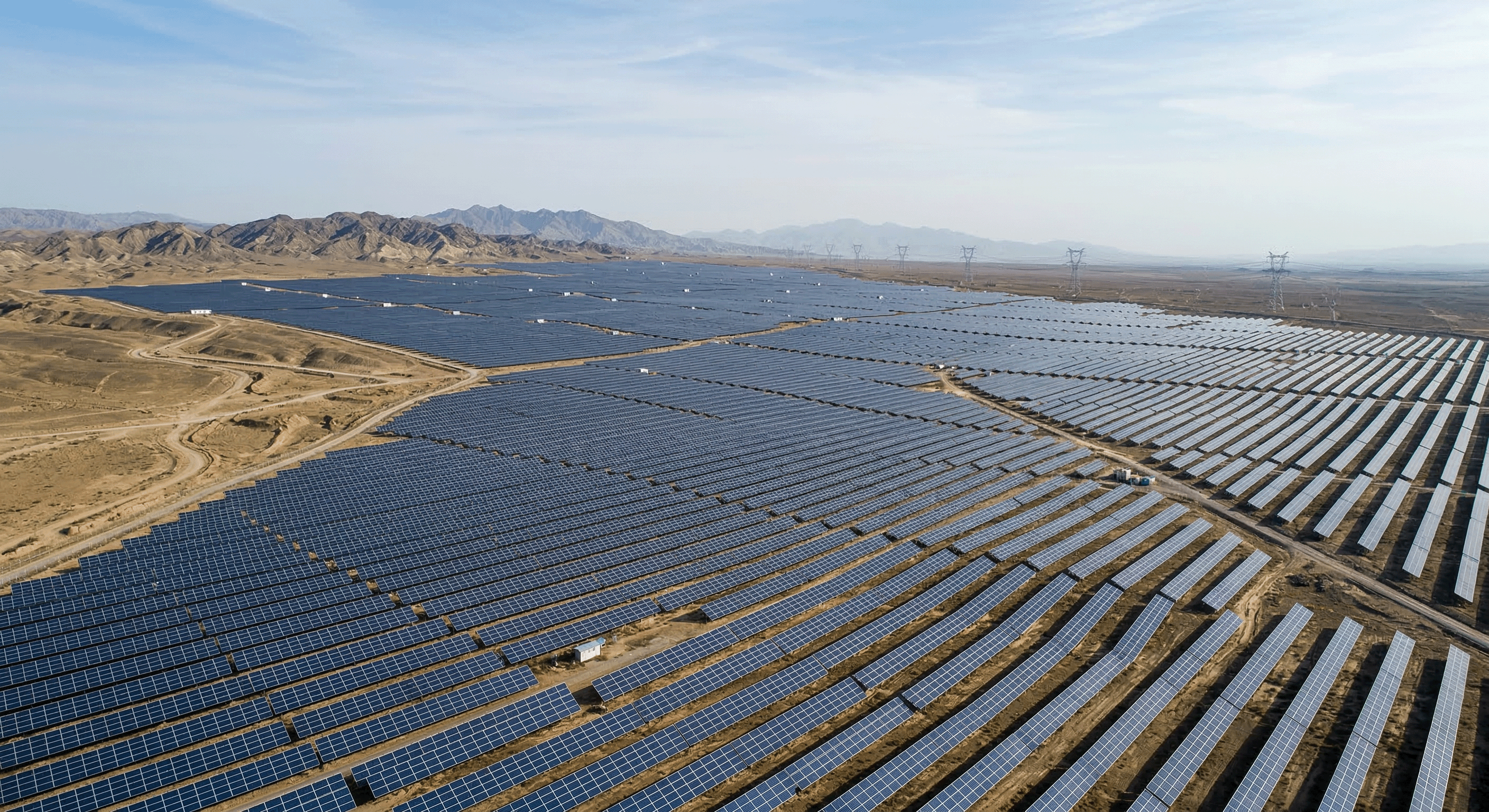

The plan commits China to raising its share of non-fossil energy to 25% of primary energy consumption by 2030, up from 21% in 2025. It sets a long-term renewable energy target of 3,600 gigawatts of solar and wind capacity by 2035, and reaffirms support for electric vehicles, batteries, green hydrogen, offshore wind and nuclear power. On paper, these are substantial commitments from the world's largest clean energy manufacturer.

However, the plan's headline climate target has drawn scrutiny. It sets a carbon intensity reduction goal of 17% over the five-year period, meaning China aims to cut the amount of carbon dioxide emitted per unit of economic output. This is lower than the 18% target in the previous plan, which China also missed, achieving only around 12%. Analysts at the Centre for Research on Energy and Clean Air note that the methodology used to calculate carbon intensity has been quietly revised to include industrial process emissions, making the target easier to reach without deeper cuts to energy emissions. Under this framing, overall emissions could still rise by an estimated 3 to 6% during the plan period.

Coal Remains in the Picture

One of the more significant details in the plan is what it drops rather than what it adds. The previous plan included language to "gradually reduce" coal consumption. That commitment is absent from the 15th plan. Instead, the document calls for coal consumption to "peak" during the 2026 to 2030 period, without specifying a year or a decline trajectory. Coal plants are to be adapted through retrofits, including co-firing with biomass or green ammonia, rather than being retired. This reflects China's stated priority of energy security alongside decarbonisation, particularly in the context of rising geopolitical uncertainty and elevated fossil fuel prices.

Industrial Strategy and Global Trade

The plan reinforces China's position as the dominant manufacturer of clean energy technologies. It explicitly backs critical minerals, solar, EV and battery supply chains as strategic industrial priorities. China's solar manufacturing capacity already exceeds domestic demand by a factor of three, meaning significant export volumes are likely to continue. This has direct implications for European industry. The EU's Carbon Border Adjustment Mechanism, which entered its definitive phase in January 2026, places a carbon cost on heavy goods imported into Europe, including steel and aluminium. The pressure this creates on Chinese exporters to reduce the carbon intensity of their products is now a live commercial consideration, not a future one.

What Comes Next

The plan approved this week is a framework. Detailed sector-specific plans covering energy, renewables, carbon markets and coal are expected in the coming months. A new "carbon dual control" system is also taking effect, which for the first time places binding emission caps on certain industries and local governments, moving beyond intensity-based targets alone. Whether enforcement follows ambition will be the central question for analysts and investors tracking China's transition over the coming years. The plan sets the direction; the sector plans will determine whether the infrastructure and capital flows match it.